Xero's US assault - analyst raises 'small red flag'

UPDATE: Drury claims success as key US rival flatters it with a mention in a market risk statement.

UPDATE: Drury claims success as key US rival flatters it with a mention in a market risk statement.

UPDATE / Sept 14: "Success! @Xero mentioned in Intuits 10-K filing," Xero CEO Rod Drury tweeted this morning.

And indeed Intuit's filing to the US Securities and Exchange Commission, accompanying its annual result, includes the following line on risks it faces in the market:

Increasingly, our small business products and services also face competition from newer online accounting offerings from companies such as Xero, free or low-cost online accounting offerings, and free online banking and bill payment services offered by financial institutions and others

Intuit's 10-K follows its /full-year result for the year to July 31, released August 21, saw the company report users of its cloud product, QuickBooks Online, increased 28% to 487,000 (with 20,000 outside the US).

That's a modest number, given Intuit completely dominates the accounting software market in the US overall.

And it makes Xero's 210,000 customers worldwide look not too shabby at all.

In earlier comments to NBR, Mr Drury stressed Xero's number is all paying business customers; Intuit's includes an unspecified number of trialists.

Mr Drury tells NBR he rates the company's first US-based event a success on the basis the Sept 4 & 5 "XeroCon" attracted 400 accounting partners - equal to the company's first Australia event last year (this year it had 900 at XeroCon across the Tasman).

Xero needs to add US payroll capability to be fully competitive in the market, Mr Drury says. A preview went down well at XeroCon.

Aug 5: Woodward Partners Securities’ Nick Lewis remains bullish on Xero. But he raises “a small red flag” in regard to the online accounting company’s crucial assault on the US market.

That red flag relates to the behaviour of Intuit, the software giant whose Quicken and QuickBook products hold around 90% of the US accounting software market, and its nascent aggression toward Xero.

Specifically, Intuit has scheduled an event to exactly coincide with Xero’s first US conference (XeroCon in San Francisco, Sept 4 & 5).

Xero CEO Rod Drury sees the timing as no coincidence.

“Hats off to Intuit for pulling the old event ambush trick … makes sense for them to hold onto their influencers,” he tweeted on July 19 as a US trade journal announced Intuit’s VIP Accounting Professionals Summit.

Another minor bit of push back has been Intuit's launch of QuickBooks Online into Australia late last year [UPDATE: Although Quicken has a near-monopoly on small business accounting in the US, in its quarterly earnings released August 21, Intuit reported a modest 487,000 users of QuickBooks Online - and it wasn't clear if all of those were paid. It's not streets ahead of Xero's 193,000.]

Two paths

The question now, Mr Lewis says, is what happens if Xero becomes a bigger fly in the ointment.

He sees two possibilities.

One, there will be “stronger push back” from Intuit, such as lowering the price of its cloud product. (There’s not a lot of scope there, with Xero allowing companies unlimited users for $US29/month. But price moves by Intuit would under-cut Xero's key aim to charge businesses on a per user basis).

Two, Intuit buys Xero.

As a profitable company with a big market cap, Intuit could easily digest the $2 billion Xero, Mr Lewis says (in 2012, Intuit [NAS:INTU] made $US767 million on $US4.1 billion revenue; it has a $US19 billion market cap).

For now, Xero has to be flattered by the attention (and certainly it’s milking it; a November 2012 investor day presentation quotes Intuit CEO Brad Smith saying of Xero: “I admire them. I think Rod Drury and the team have built a really good company, they have built a very easy and compelling product. We've learned some things from Xero that are helping us think differently, which is the highest compliment you can pay to someone who competes in your space").

Xero also made it to a highlight box in a Fortune magazine piece on David vs Goliath fights (a snippet of which is aggregated on a Time Warner site here).

“American’s love a David and Goliath” fight,” Mr Lewis says. "It's fantastic free publicity."

Certainly, all Intuit has achieved by short-notice scheduling its own event against XeroCon is to give the Kiwi contender headlines (at least in the accounting press). After years of Intuit's nearly monopoly, there must be a few American scribblers who'll welcome the chance to write about a fresh contender.

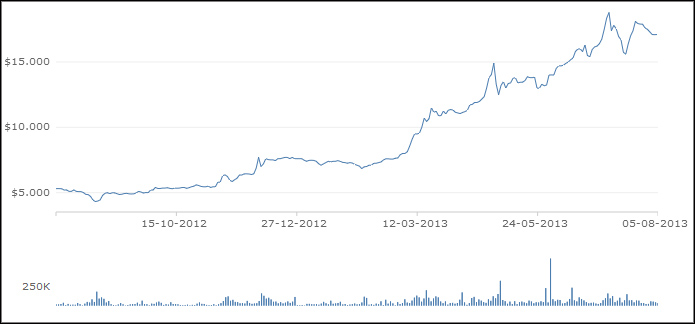

ABOVE: Xero 12-month price history (NZX.com)

Ecstatic - but where to from here?

Mr Lewis says shareholders Xero’s annual meeting last week were among the most upbeat he had ever witness. The mood was “enthusiastic, even ecstatic.” (Acccording to Brian Gayor's account, the only darker note was when Mr Drury "criticised the National Business Review for its negative views on the company." For the record, I think Rod Drury is a smart guy, and Xero is a great company. Whether it's $2 billion worth of great is a separate question, and one that great deserves robust discussion.)

I’d have to say I’d be pretty ecstatic, too, if I’d bought Xero shares six months or a year back.

But it’s easy to bet on yesterday’s horse race.

The question is, where are Xero’s shares heading to from here?

After last week’s cashflow updated, Forsyth Barr downgraded Xero from hold to reduce, saying while it believed in the company’s long term growth plan, its future success was already priced into the stock.

In December 2012, boutique Woodward Partners put a 12-month target of $12.00 on Xero, and Mr Lewis was the only analyst with a buy rating on the stock (Forsyth Barr, the only major brokerage covering it, had a hold). It seemed ambitious at the time given shares were trading at $7.70 (on June 4 this year, as Xero closed at $14.01, Woodward upped its target to $16).

Woodward has yet to update its “buy” rating since last week’s Xero update (Mr Lewis is now covering the stock for Woodward Partners Securities, spun off from Woodward Partners the boutique investment bank).

But he did share that he was heading in the direction of “accumulate” which he described as a rating between “buy” and “hold”.

He says he’s not concerned about Xero’s increasing cash burn, given its easy access to capital from sophisticated US investors like Peter Thiel.

And he sees annualised revenue hitting $87 million in Xero’s 2014 financial year – or 100% growth (as opposed to the “over 80%” figure given by Mr Drury at the AGM - a figure that the CEO was more bullish on in his later comments to NBR).

If Xero does hit that mark, he sees a possible move in its share price to $20 to $25 (an off-the-cuff observation to NBR; as noted he’s still working on his post-cashflow update report and formal figures). Long term, at its current rating, Woodward sees Xero with a market cap of $6.4 billion by 2019.

A move to $20 - $25 sounds ambitious, but remember Woodward underestimated the surge since March. That would be a stonking result for shareholders, and New Zealand as a whole. Now, let’s just see how Intuit chooses to push back …

MORE:

Xero CEO Rod Drury tells NBR Quicken has "a complete lock on the US" but also calls it complacent, and offers his take on its limited cloud subscriber numbers. Plus: why was Xero shy of revealing US customer numbers in its latest update? Read Drury discusses that lower growth forecast - and Xero's monolithic competition in the key US market.

Forsyth Barr's Broker calls Xero 'inspirational', but busts it to sell