Xero hits $1.58b market cap, Woodward sees it climbing to $6.4b

PLUS: Company offers software developers a $10,000 signing bonus.

PLUS: Company offers software developers a $10,000 signing bonus.

Xero shares [NZX:XRO] rose 6.88% today to hit another new high of $13.20 in late trading, valuing the company at $1.58 billion.

CEO Rod Drury told NBR Online that recent developments across the Tasman have helped buoy the stock.

These include Deloitte choosing to to sell Xero after a competitive process that included assessment of incumbents, and rumours in the AFR that regional rival MYOB may soon have its third change of ownership in four years.

The $1.58 billion market cap will re-ignite talk that the online accounting software company's valuation is running ahead of its growth.

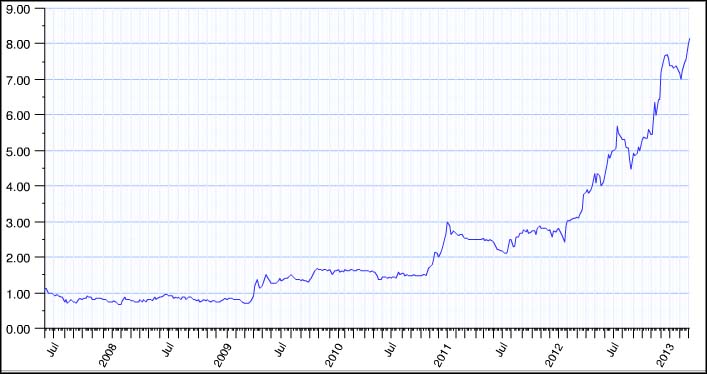

After Xero's April 5 update to the NZX (below), Forsyth Barr hiked its 12-month price target from $6.35 to $12.50.

But the broker assessed the stock as "speculative" and retained its hold rating.

XERO: 12 months to March 31, 2013

Bottom line: $15 million loss (year-ago: $7.9 million loss)

Revenue: $39 million (year-ago: $19.4 million)

Cash: $71 million (year ago: $38 million)

Paying customers: 157,000 (year ago: 78,000)**

Staff: 382 (year ago: 174)

Market cap: $1.52 billion

* All figures from April 5 NZX update for 12 months to March 31, 2013. The update forcasts a full-year loss "under $15 million." The update says monthly subscriptions are now at a rate that implies $51.5 million annual revenue.

** NZ: 73,000 (year: ago: 47,000; +55%)

Australia: 51,000 (16,000; +219%)

UK: 22,000 (11,000; +100%)

US/global: 11,000 (4,000; +175% )

Mr Drury professed not to be watching the share price, at least today.

Instead he has been using social media to push a new $10,000 signing bonus for new software developers (essentially, its footsoldiers) as Xero looks to hire 200 to 300 new employees this year (its current total is 382).

The company is looking "to nudge a few people into approaching us," the CEO says. An ongoing IT skills shortage sees the online accounting company in competition for staff with the likes of Orion Health and Trade Me. There's also an element of avoiding recruitment company commission (you have to come to Xero direct to claim the cash).

Mr Drury says he's looking to thicken up the Wellington-headquartered company's development team in New Zealand; especially in Auckland where it recently opened a second office. But around half the new hires will be made offshore, where the focus is on recruiting sales staff.

In the key US market - where Xero recently reported a modest sub-11,000 customers - the company recently created Northern and Southern California sales teams.

The company will hold its first US "Xerocon" conference in San Francisco in September in an effort to piggyback on the America's Cup, and join Moa and other NZ companies participating in NZTE promotions around the event.

Xero's US headquarters has always been in San Francisco, but it recently moved out of the Kiwi Landing Pad and into its own office.

Analysts who have seized on a possible Xero Nasdaq listing as a justification for its sky-high stock will be keeping a close eye on the action in California, and Xero's broader push into the US.

Mr Drury recently told NBR he had received advice that a Nasdaq listing could make sense once the company hit the $US100 million revenue mark.

As Xero hits $1b, banker sees it heading for $6.4b amid Nasdaq talk

UPDATE / March 8: Xero shot through the $1 billion market cap mark yesterday as shares [NZX:XRO] closed at $8.59 (in midday trading today they had edged up further to $8.60).

The milestone reanimated debate (below) over whether the high-growth company can live up to the heady promise of a 10-figure market cap.

For Wellington's Woodward Partners, the answer is not just yes, but hell yes.

The boutique investment bank has written a research report with a 12-month price target of $12.00 - which would push Xero's market cap to $1.4 billion (by contrast, Forsyth Barr has a hold rating and a 12-month target of $6.32).

But wait, there's more.

Woodward says by 2019 Xero shares could reach $55, valuing the company at $6.4 billion. At that time it predicts Xero will have 4.2 million customers.

At this point, some readers will be making bubble popping sounds (and perhaps ruder sounds if they recall Woodward's bullish comments about a Charlies-style takeover ahead of Energy Mad's October 2011 IPO. The company's shares listed at $1. Today they're trading at 35 cents).

But here's the bank's thinking: you should value Xero like a venture capitalist.

Xero may have been "Unprofitable since its founding in 2006, and with no profits on the horizon" as Woodward puts it, with a P/S ratio of 20 "is normal behaviour for companies with a five-year CAGR [compound annual growth rate] of 222% and chasing a global opportunity." In a larger financial market, Xero would have been financed in the venture capital market.

Nasdaq listing seen

Woodward also boldly predicts Xero will list on the Nasdaq within two years, raising around $300 million (the company has already expanded to a dual listing on the ASX, where it debuted in November last year).

NBR ONLINE put this to Mr Drury.

"It’s certainly something we think about," the Xero boss said.

"We haven’t made any formal decision but it’s something for us to consider. If you think about building a global brand, that’s something that would be part of the playbook."

The company is looking at a potential Nasdaq listing in terms of a revenue rather than time.

Advice Xero has received is that a North American listing makes sense once a company hits the $US100 million revenue mark, Mr Dury said.

A walk in the clouds

NBR agrees with Woodward that the US market is key to Xero's success, and that it has a shot of becoming one of the top four accounting software vendors in that market.

There emergence of cloud computing is rewriting the rules in many markets. The move to internet computing has let to many company's reviewing their computer systems, giving newcomers like Xero a foot in the door.

But no amount of financial modeling, or analysis of industry trends so far, can tell us whether Rod Drury and co - smart cookies that they are - will succeed in reaching a tipping point in the US as they schmooze their way around industry events and accountant conferences, partner up and otherwise finagle into the North American market. Or whether incuments will get their finally act together, or insurgents suddenly appear over the horizon.

March 7: Just eight months after NBR asked, "is Xero worth a cool half billion?", Rod Dury's online accounting software company has hit a $1 billion market cap.

In late trading, Xero shares were up 5.04% to $8.55 - lifting the company's value to $1,001,958, or a $70 million increase on the day.

In a February 7 update, Xero said it had more than 23,000 customers to its client list since September and says it is on track to double last year's $19.3 million in annual revenue.

The Wellington-based company has more than 135,000 customers and monthly recurring revenue of almost $4 million, it says in a statement. That implies annual sales of some $48 million.

Xero CEO Rod Drury has long maintained it is better to push for growth than profit at this phase of Xero's existence.

Over the same period, cash has increased from $38 million to $85 million - primarily thanks to December capital raising round that sawy Peter Thiel-backed Valar Ventures of San Francisco invested $24 million and Massachusetts-based Matrix Capital Management invest $58 million. They also bought collectively $22 million of existing shares from Xero's three largest shareholders: Mr Drury, co-founder Hamish Edwards and director Craig Winkler.

Xero NZX performance since IPO (S&P Capital IQ. Click to zoom).

Despite Mr Drury offloading some of his holding during the December round (it now stands at 18.3%), he and his fellow managers and employees still have a lot of skin in the game.

Xero has about 3000 shareholders and 48% of its shares are held by directors and staff, according to the January 31 filing.

Following Xero's half-year result, Forsyth Barr reiterated its hold rating, and put a 12-month price target of $6.32.

"On normal valuation metrics Xero appears fully priced," the company said in an update.

"However, at this stage the share price is still not so high as to be pricing in unreachable targets. Our analysis suggests it is pricing in Xero reaching around 1.1 million customers in approximately five years."

By any conventional metric, Xero's valuation is off the charts. But major December cash injection shows the stock's appeal to sophisticated tech investors, ForBarr says.

Some are no doubt hoping for a trade sale, as with Mr Drury's previous two start-ups.

The Xero boss says he's in it for the long haul, but is also not above pointing out tasty trade sales, as in this tweet:

Another $B+ enterprise SaaS exit zdnet.com/cisco-acquires… White hot space

— Rod Drury (@roddrury) November 19, 2012

Mr Drury kept things low key when approached by NBR OLINE for comment this afternoon.

"It's a cool milestone but still lots of work to do," he said.

Sign up to get the latest stories and insights delivered to your inbox – free, every day.