Xero can win - First NZ analyst models share price scenarios from 'US fail' to 'US Blue Skies'

Broker models customer scenarios from “US fail” to “US Blue Sky” and what they mean for the software company's share price.

Broker models customer scenarios from “US fail” to “US Blue Sky” and what they mean for the software company's share price.

A new analyst report paints seven customer scenarios for Xero - each turning on its degree of success in the crucial US market - and what those mean for the super-hot tech's already heated share price.

Some are rosy. A couple are pretty ugly.

But before we get to that:

Will Xero win in the software market?

I think it’s likely.

In the US, it faces a monolithic incumbent, Intuit – whose personal finance (Quicken) and small business accounting software (QuickBooks), hold a near-monopoly.

But Xero’s been in this position before in Australasia, against MYOB, and the UK, against Sage.

In both cases it didn’t spend a cent on traditional advertising, instead assiduously courting accountants, who in turn influenced the software chosen by their clients.

Along with smart use of social media (both for general boosterism and stealing customers) and frequent media appearances this strategy has created buzz around Xero’s pure-play cloud software at a time when MYOB, Sage and other established players are juggling online and offline products.

The situation is different in the US. Where MYOB made a net loss last year and is lumbered with $A693 million in debt, Intuit (market cap: $US20.5 billion) made a net profit of $US858 million on revenue of $US4.2 billion in the year to July 31, 2013. It has just over $US1 billion in the bank.

You could spend almost limitless amounts of money trying to break into the US. But Xero’s strategy of courting accountants at its own events (it has a roadshow making five stops in California this week) and trade conferences is relatively low-cost.

And even CEO Rod Drury’s tactic of working the press is lower cost than usual. There’s no PR company engaged, or buying ads that get you (cough) on the radar. Rather, Drury is simply good at making news, and is always on the end of the phone. Crucially for Xero (and any shareholders wondering what happens if Rod gets hit by a bus), the company’s US-based President, Jamie Sutherland, is no slouch on this front either, having recently garnered coverage in Fortune magazine and on Bloomberg TV, among other appearances.

Drury has gathered smart people around him. He’s consistently proved good at picking trends. His plan to add new front-office modules to Xero (such as HR) is a good one, and the company’s strategy of creating an eco-system of apps around a Xero platform is solid, and seems to be gathering momentum (on October 3, Xero said the number of add-on applications globally is 300, up from 160 a year ago).

Cash burn is high – $9.4 million in the June quarter and $14 million in the September quarter – and accelerating as Xero piles on staff (the company has around 600 and is in the process of adding another 100; Drury says numbers could double over the next year).

But where MYOB has to list interest-bearing debt to raise funds, Xero’s high and rising share price practically gives it access to free money. On October 14 it raised $180 million by issuing just a handful of new shares – which of course did not have any diluting effect (the new shares were bought at $18.15; a premium; the stock went into a trading halt at $17.95 before the announcement. Since then, Xero shares have been on a tear, peaking at $41.50 this week for a market cap above $5.3 billion before settling back to $35.21).

The new funds – which take its total cash to $230 million – give Xero time to succeed. And as Drury has told NBR, his company is currently “fighting with one hand behind our back” in the key US market. It won’t add payroll modules until the New Year.

Drury readily acknowledges Intuit has a tight grip on the US market. Various surveys give it between 80% and 90% of the small business market (an oft-quoted figure is that there are 29 million small businesses in the US, although Quicken hasn’t given any detailed figure on the number of companies that use its software; and of course many smaller companies and sole traders will simply be cobbling things together in Excel, or otherwise using no accounting software).

But when you focus on the high-growth area, the cloud, things look a little rosier Xero.

Intuit's August 21, 2012 Nasdaq filing, for its financial year to July 31, released August 21, saw company report users of its cloud product, QuickBooks Online, had increased 28% to 487,000 (with 20,000 outside the US).

That means Xero – with an 89% annual increase to 211,300 customers (according to an October 3 NZX filing) – is well within cooee. And more so when you consider Xero’s number is all paying customers, while Intuit’s 487,000 includes an unspecified number on a free-trial period.

It’s important not to over-state Xero’s current position in the crucial North American market. According to its October 3 filing, under 16,600 of its customers are in the US (that’s the number listed under “US/Rest of World; of the three markets where specific customer numbers are given, NZ has 85,500, Australia 79,100 and the UK 30,100).

And Xero’s revenue figures also reflect that, so far, it has only a toehold in the US, Annualised monthly subscriber revenue at September 30, 2013 was $70.6 million, which was made up of New Zealand $23.9 million, Australia $30.2 million, UK $10.2 million, and US/rest-of-world $6.3 million.

As Xero builds on its sales and sales support staff in the US (it has 100 staff across San Francisco, LA, New York and Denver), it’s going to gain more traction.

Even before its first “XeroCon” conference in the US in October, 2000 US accountants have completed Xero training events, the company said at its AGM. The largest accounting firm in California (and the 29th largest in the US), Armanino, has signed on as a partner.

Xero has landed a five-star review in CPA Practice Advisor, and been talked up by influential tech blogger Rober Scoble (aka @Scobleizer), albeit in his day job at Rackspace, Xero's data centre host (hey, you've got work every angle).

The company’s cash rich, it’s got a solid strategy, and its grafting hard. And arguably, the fact Intuit’s still making good from its legacy software will work in Xero’s favour. A complacent incumbent, tied by golden handcuffs, could be rich pickings.

Xero’s already a great NZ success story, and it’s hard not see it continuing to pile on customers and become profitable.

ABOVE: A panorama Xero's new office in San Francisco - a 25,000 square foot space where 75 of its 100 US staff are based (via @RodDrury; click to zoom).

Can Xero win on the stock market?

I have no idea.

In June last year, as Xero’s market cap approached $500 million, NBR asked Is Xero worth a cool half billion?.

Some people were using the word "bubble" by that point. I don't know what the word is to describe what's happening now, with Xero [NZX:XRO] passing the $5 billion market cap milestone this week (before settling back a little).

Since that "half billion" article, as mentioned above, Xero has grown customers 89% to 211,300, and has seen an attendant growth in its annualised revenue to $70.6 million (the company says its 2014 loss will be wider than the prior year’s $14.4 million; as noted above it now has $230 million in cash, and a burn rate last quarter of $4.6 million a month).

But its share price has accelerated far beyond the point where you can apply any traditional valuation metric like price-to-sales or price-to-earnings.

As it topped $5 billion market cap this week, Xero became the NZX’s second most valuable company.

Investors can take heart that a sophisticated investor like Peter Thiel (PayPal co-founder, the first outside to put money into Facebook and an early backer of Yammer and LinkedIn) re-upped his investment in Xero as his investment company participated in the October 14 $180 million capital raising round at $18.15 (although a penny for his thoughts as Xero hit $41.50 this week).

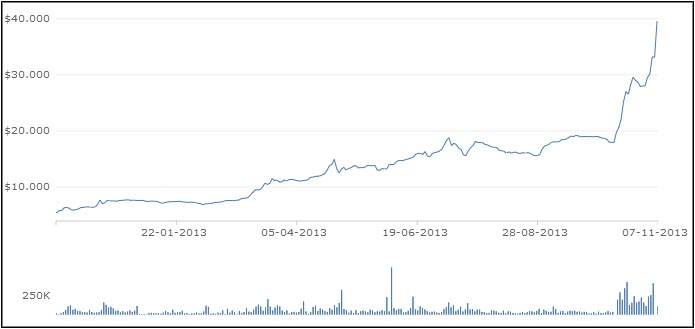

ABOVE: Xero one-year price history (NZX.com)

Clearly, investors are taking a punt on Xero’s potential.

There’s potential for Xero to be bought.

Intuit and Sage (which came close to buying MYOB last time it as up for grabs in late 2011) are obvious candidates. There would be a lot finger-drumming on the boardroom table if loss-making Xero up for grabs at its present valuation. But another couple of years of doubling customer growth - especially in the US – could shift thinking.

Intuit has already shown a modest appetite for acquisition picking up cloud-based personal finance outfit Mint.com for $US170 million.

Drury says Xero is not up for sale. But then again he sold his first two companies, and if the price is right, anything is for sale.

Of course, Intuit could also push back, and invest more in QuickBooks Online.

Scenarios from "US fail" to "US Blue Sky"

This week, First NZ Capital became the second major brokerage after Forsyth Barr, to initiate coverage on Xero.

First NZ research analyst James Schofield rates Xero a buy, with a 12-month target of $47.50 (ForBarr has a hold rating and a 12-month target of $20.30).

Both brokerages (and the smaller Woodward Partners) see US success as the key to justifying Xero’s heady valuation.

In its first research note, First NZ models Xero’s share price against seven possible customer scenarios, seven years in the future.

The worst-case FY20 scenario is “US fail”, which sees 1.6 million worldwide customers, valuing shares (close your eyes, those who bought in this week) at $13.50. First NZ sees a 10% chance of this scenario.

“US traction”, rated a 35% probability, sees 4.3 million customers in 2020, valuing shares at $43.48.

“US success”, rated a 20% probability, sees 5.6 million customers, valuing shares at $58.50.

And the go-go “US Blue Sky” scenario, rated a 10% probability sees 7 million customers, which First NZ ses valuing shares at $75.55.

(First NZ uses three different valuation methods, but all the results are quite close. I’ve quoted a selection of its DCF numbers; see a primer on how a DCF valuation is calculated here.)

First profit seen in FY2017

First NZ sees Xero making increasing losses, culminating in a $49 million loss in FY 2016 (the year it anticipates Xero will hit 1 million customers.

It sees the first profit in FY2017, with Xero making $37 million profit as customer numbers pass 1.75 million, followed by $238 million profit in 2018 as customer numbers pass 2.6 million and revenue hits $1 billion.

Nasdaq listing seen as transformative

Mr Schofield tells NBR part of this week's huge Xero run-up was driven by an increasingly number of US and Asian investors coming onboard the NZX and ASX-listed Xero.

But like all analysts NBR has spoken to, he sees a Nasdaq listing as key component of future success. It will boost Xero's profile (and, yes, hype) as well as providing a direct line to the world's most active tech investors.

Drury earlier told NBR that Xero has taken advice about issues related to listing on the Nasdaq; it was told a US listing would make sense once his company hits $US100 million in annual revenue.

First NZ sees Xero hitting that mark in 2015.

Certainly, an ASX/NZX listing would start to bust at the seams is Xero does hit the "Blue Sky" scenario First NZ paints as a possibility.

Salesforce - the pioneer and poster boy for software-as-a-service software - today has 100,000+ customers (lower than Xero, but many are large corporate accounts) and lost $US270 million on $US3 billion last year. Like Xero, it disrupted its industry. If Xero achieves similar revenue and customer success, then it's not outlandish for it to garner a $10 billion market cap on the Nasdaq by the end of this decade (Salesforce has a $US33 billion market cap). But it's harder to imagine it hitting that mark if still contained to ASX/NZX.

Those qualifiers in full

Drury has not commented on 2015 revenue, when Xero could make a profit, or whether it will list on the Nasdaq – beyond acknowledging that is one of the options on the table.

Despite First NZ’s $45.70 one-year target and generally bullish numbers, Mr Schofield – like his opposite number at ForBarr – emphasises that Xero is a speculative play. It suits sophisticated investors who acknowledge the risk along with the potential rewards, and the usual rules about a diversified portfolio apply.

“As with any tech company going global, risks are extreme. Xero faces able competitors, especially Intuit. Risks include: execution, competitive response, key man [Rod, look both ways before you cross!], security, and high market beta,” First NZ warns.