The first day of October has dawned and with it the introduction of the loan-to-value (LVR) restrictions imposed by The Reserve Bank on the main trading banks forcing them to reign in their lending to borrowers with low deposits (less than 20%).

Certainly this is going to have an impact on the property market. It will impact those who either do not have the necessary 20%+ deposit and also importantly those who do not want to tie up that much capital in a property, especially an investment property. Investors tend to like to highly gear their investment properties so as to maximize their interest cost recovery against tax. Therefore there will likely be an impact not only among first-time buyers but also investors.

However as with all matters economic, there is always a contrary position and in fact there will be winners or potential winners from the LVR restrictions.

The fact is the main trading banks whilst strictly adhering to the new policy (especially as their operating license is at stake, not something they are likely to risk for one second) will not for a moment relinquish their desire to continue to build their business by lending against property as a secure asset. These banks are hardly going to be able to settle back and report to their shareholders that they have seen their profits fall because of this policy. Their shareholders will rightly expect them to seek to find alternative lending options to make up for any potential loss of clients in the high LVR market.

This is where that contrary position comes in. If you are not a first-time buyer or an investor. If you have a healthy equity ownership in your property and you are possibly looking to buy a house or refinance. You may well now find out that your local bank is even more happy to see you, greet you warmly and encourage you to discuss options with you.

The fact is that for every large value low-LVR mortgage that a bank can write, will effectively allow them to offer a lifeline to first-time buyers and investors.

Here is a somewhat simplistic example to illustrate this situation.

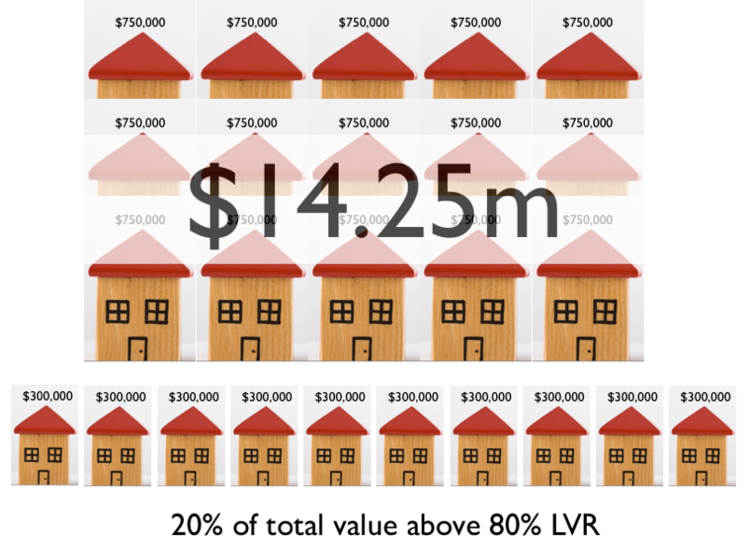

Lets say a bank as of last week has 25 prospective mortgage customers. 10 of those customers are after a 90% mortgage to buy a property and they all want to borrow $300,000 to fund that purchase of a $333,000 property. The other 15 customers happen to be customers with a larger portion of equity. They are looking to borrow $750,000 each to buy a $1.25m home – 60% LVR mortgage.

Click any image to zoom.

This package of mortgages totals $14.25 million and results in the bank having 21% of its mortgage book in loans over 80%. A situation that the Reserve Bank says has to stop from the 1st October.

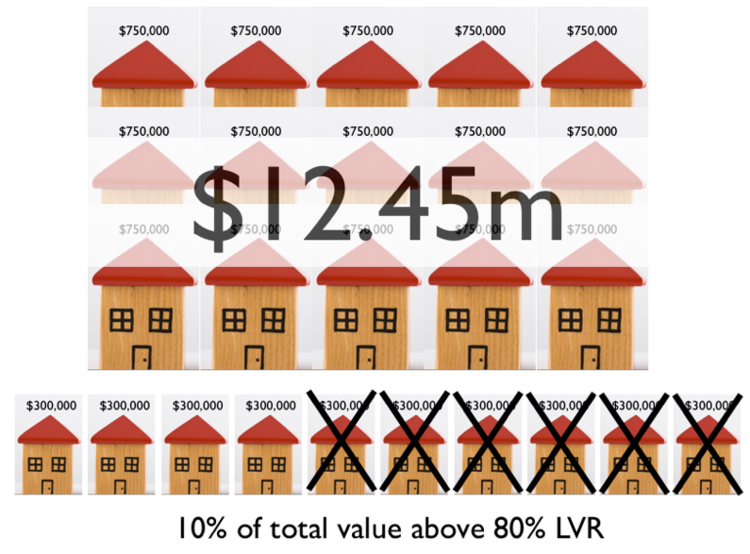

So from the 1st October the bank in the same scenario of those 25 new customers would have to turn away 6 of the 10 customer who wanted 90% mortgages to ensure that their total mortgage book has no more than 10% in high LVR mortgages. This decision would cost the bank a 13% fall in overall lending, down to $12.45 million and likely a consequential fall in profits.

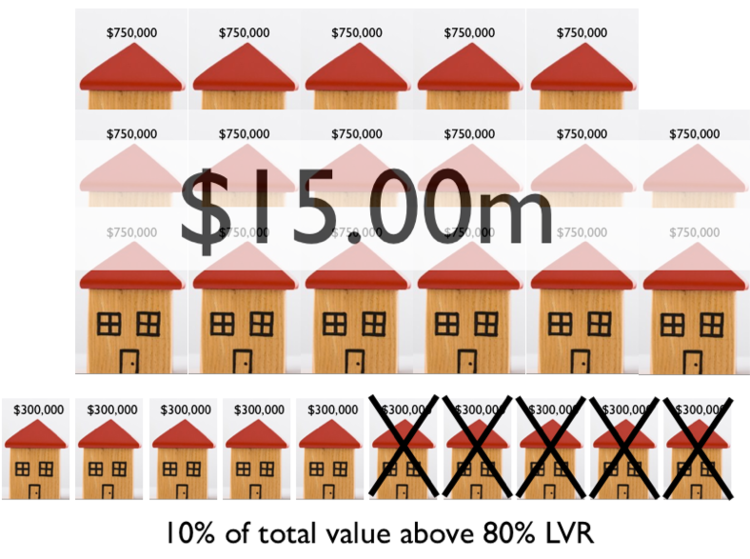

However if the bank reached out to some more of these higher value customers who are well below the 80% LVR threshold and offered them an enticement in the form of lower interest rate or other inducement then by attracting just 2 more of these higher value customers they could also satisfy one more first home buyer and in so doing end up with 22 customers rather than 19. They would have a total mortgage book up 5% at $15 million and a potential competitive advantage.

So my advice is be alert to some very friendly and generous bank representative courting you if you are after large mortgages and if you have a good strong equity position in your home!

Former Realestate.co.nz CEO Alistair Helm is founder of Properrazi.co.nz.

Alistair Helm

Sun, 06 Oct 2013

Sun, 06 Oct 2013

© All content copyright NBR. Do not reproduce in any form without permission, even if you have a paid subscription.

The silver lining of the new LVR restrictions

32792