The future of food exports from NZ

Lance Wiggs on NZ's food exports - with special audio feature.

Lance Wiggs on NZ's food exports - with special audio feature.

Click the NBR Radio box for on-demand special feature audio: Lance Wiggs on the future of food exports

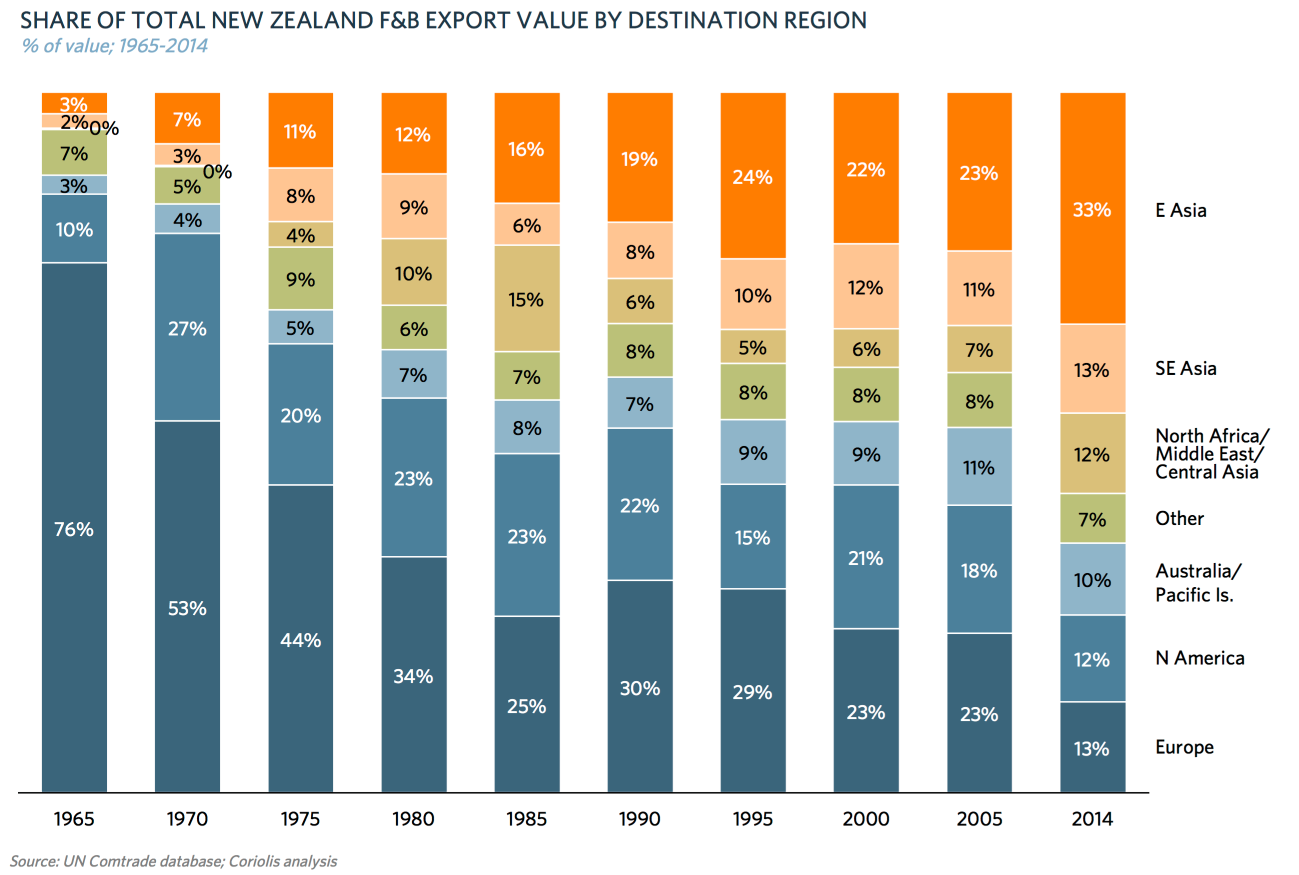

In the past 50 years New Zealand has done a wonderful job of diversifying its export markets for food and beverages, a process somewhat forced by the UK joining the EU in 1973.

We are in a strong position.

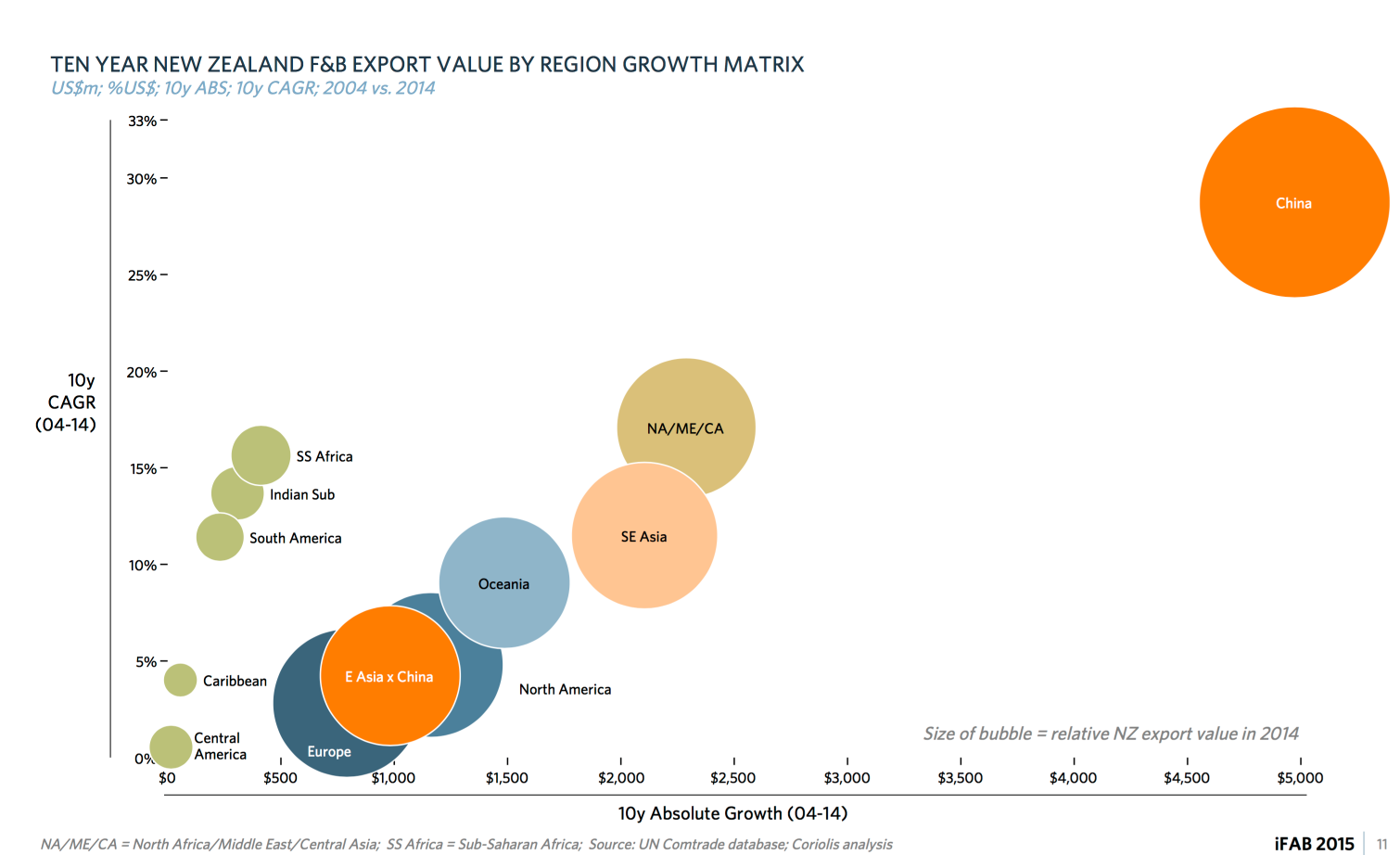

China is the biggest growth market for us – in both dollar and in percentage terms.

It has been a wonderful story of the benefits of the country's very early free trade agreement with China.

(Click to zoom)

(Click to zoom)

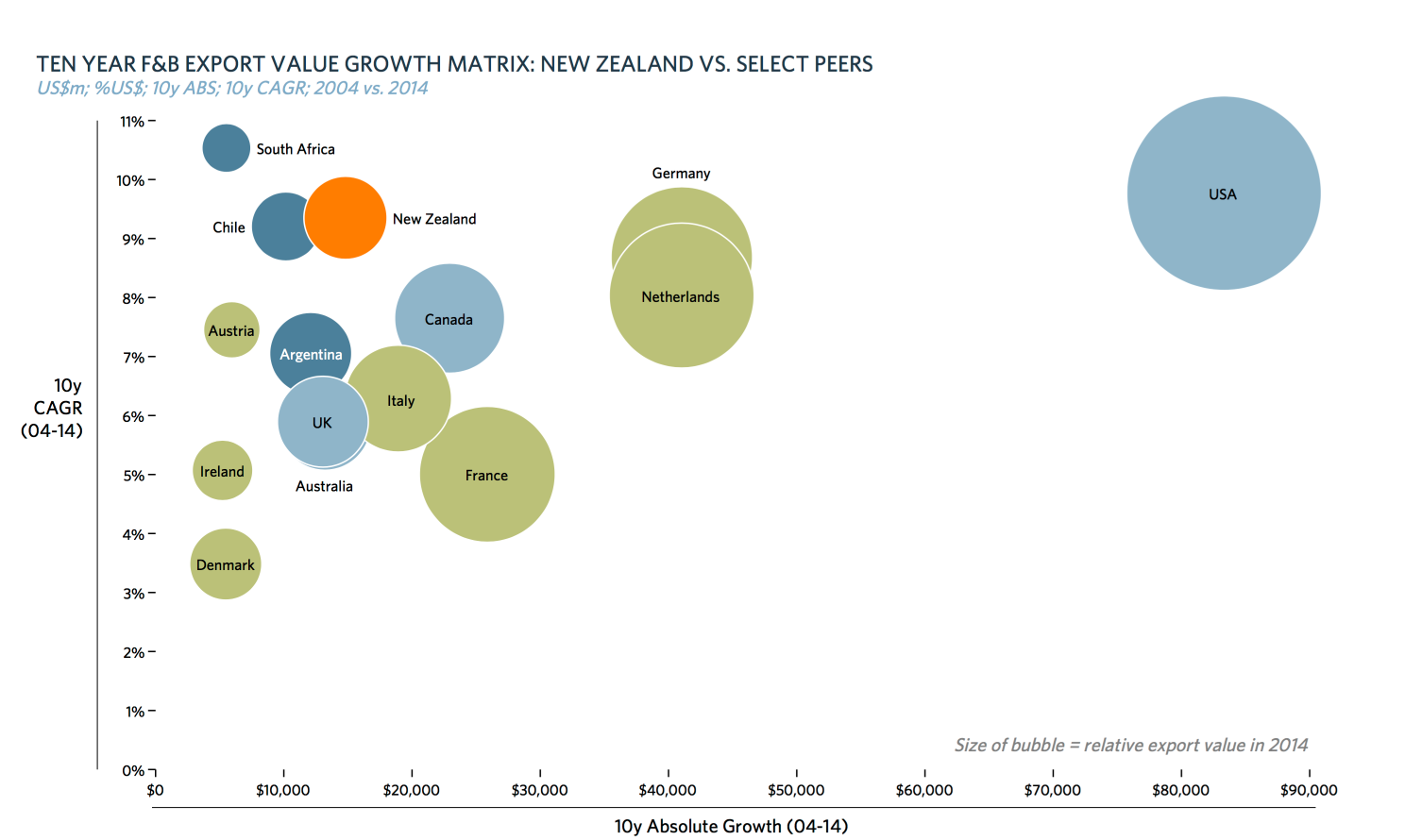

We are not the only food producer of course, and the giant exporter to worry about is the USA. Its absolute and percentage growth rate of exports is vast, and with TPPA the US now has the ability to break open markets.

In dollar terms the TPPA, which does not deal with Amercia's massive trade-supporting farm subsidies, will mainly be for the benefit of them.

(Click to zoom)

The USA’s food system is largely one of production prioritised over quality, with hormones and antibiotics added to animals producing meat and milk, subsidised corn and sugar quotas leading the prevalence of high fructose corn syrup (HFCS) and obesity, poor health and antibiotic resistant bugs.

New Zealand can’t hope to compete on quantity with the US, and while our food quality is still pretty good, one downside of these trade agreements is that people here will increasingly be offered cheaper, poorer quality food sourced from offshore. That will lead to inferior health, which, in turn, will result in poorer economic conditions.

We can, and should, maintain and even lift our food quality standards – but can we do so under our free trade agreements?

An infamous example is Mexico being forced to open its soda market to the subsidised and cheaper HFCS sweetener. Meanwhile the US fiercely protects its own sugar producers, largely because of expat Cuban sugar growers in Florida – who wield great political power.

This is at great expense to their people – with prices of refined sugar 95% higher than global prices, and along with the subsidised HFCS that means cheaprer product has a large market share as a sweetener in US processed foods.

The eventual result between Mexico and the USA was a negotiated settlement whereby the US largely maintains its highly protected sugar industry and Mexico still copes with HFCS imports and substitution of sugar for HFCS. A close read of the article on the settlement makes is somewhat disturbing as we consider the impacts of TPPA.

All these fascinating charts come from the MBIE-funded Coriolis Investors Guide to the Food and Beverage Industry, a worthwhile effort.

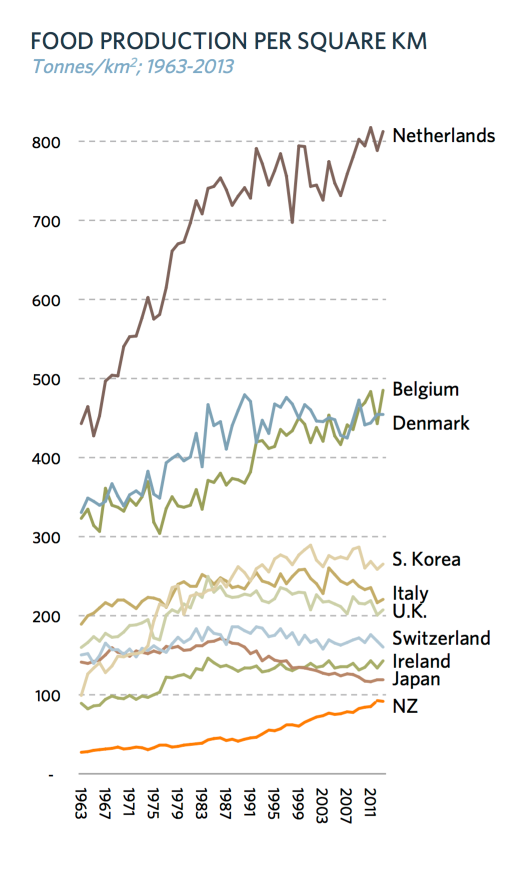

However, it is a little misleading when assessing New Zealand’s potential to increase food production. For example, the chart below compares food production per square km between countries with varying demographics, geography and protected lands. (Other charts show production per population – again not a useful metric).

(Click to zoom)

The key differences between the Netherlands and New Zealand go beyond our rugged terrain and highest point of 3726 metres versus the famously flat Netherlands and a highest point of 894 metres.

The Netherlands, data from the World Bank shows, has just 11.1% of land covered by forest, but New Zealand has 38.6%. Meanwhile 38.6% of land in the Netherlands is arable, while New Zealand has just 2.1%. Are we to chop down forests?

I do not doubt that we can get more production out of New Zealand, even if we don’t touch the forests. But that will need to be balanced with efforts to increase positive environmental effects and margins, and our resources are not as limitless as the chart above implies.

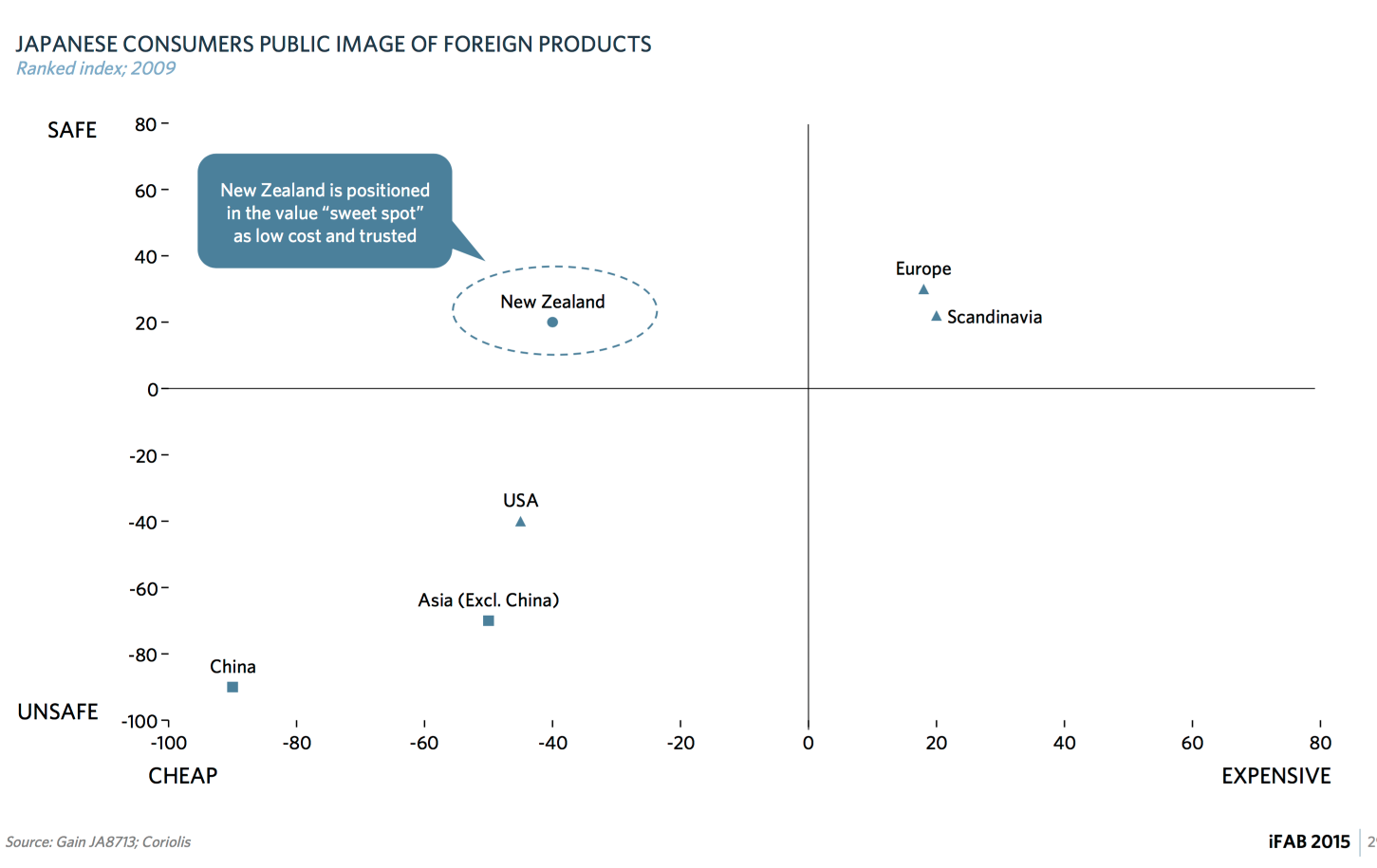

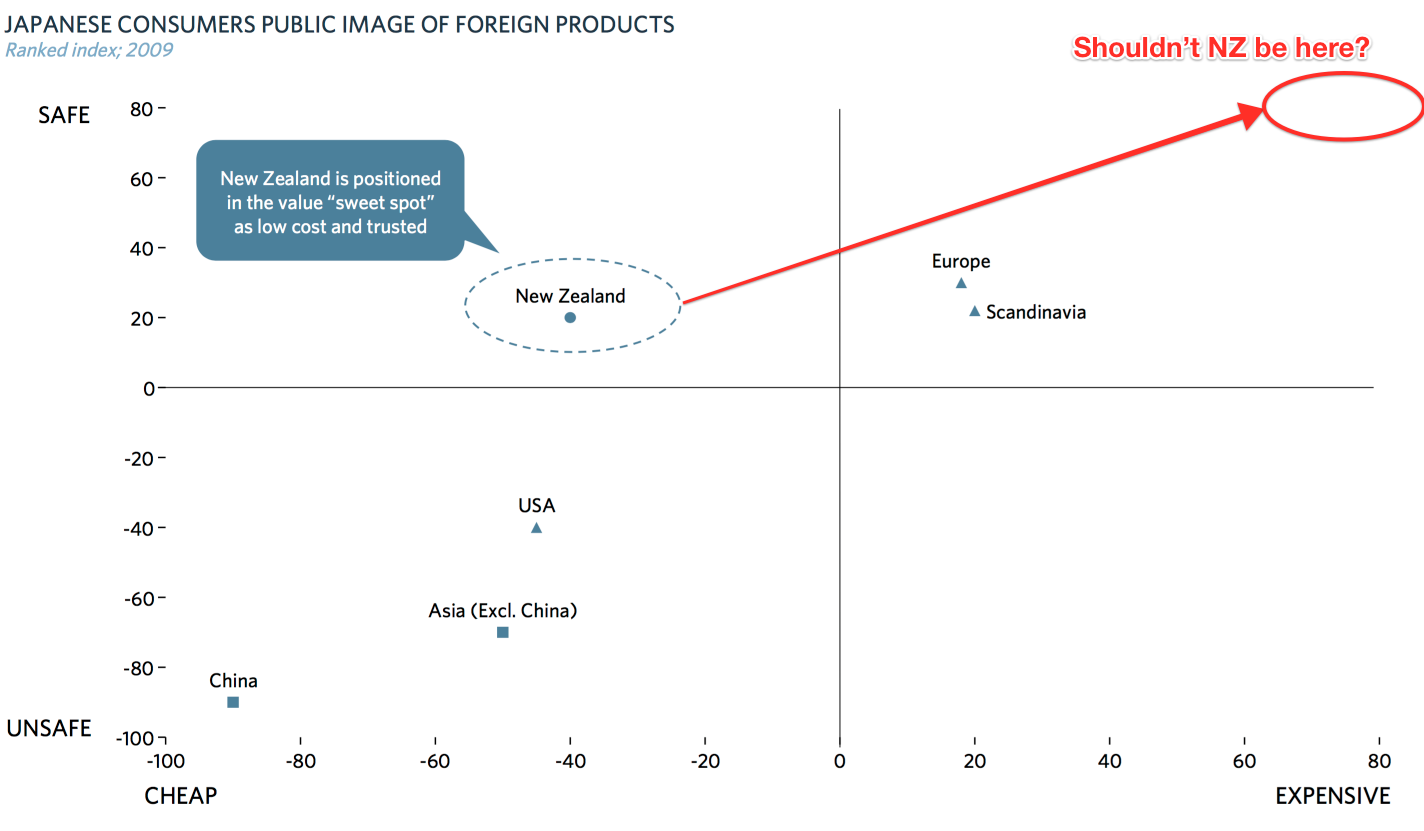

Out food is seen as cheap and safe by markets.

(Click to zoom)

This is a problem but a good one. It shows the opportunity to receive considerable margin by moving to the prestige position.

(Click to zoom)

How do we do this? The answer starts at the farm.

My favourite case study recently is Lewis Road Dairy, which charges outrageous amounts for its milk products sourced from an organic farmer. The company's products are often sold out, and Fonterra eventually responded to Lewis Road by providing its own Puhoi branded organic milk.

That’s good news for everyone, and now the real switch needs to happen at the farm level – with higher prices for organic milk (or milk/meat without palm kernel feed) encouraging farmers to switch their behaviour.

These higher quality products sell locally and globally at super-premium prices, and there is considerable potential for New Zealand to capture and own the space globally.

What can we do as consumers?

As consumers we should demand quality foods, and we should be asking or insisting that our food quality standards remain high. Let’s not allow hormone-filled meat into New Zealand, or dairy products produced by cows stuffed with antibiotics.

Let’s reward good behaviour, for example, by supporting McDonald's efforts to increase its food quality, by paying more for organic (and much tastier) food, and even switching supermarkets, as we did from the sadly declining Victoria Park New World, when high quality food disappears from shelves.

What can we do as investors?

TThis is something that entrepreneurs and investors can get involved with. Lewis Road, Firstlight Foods and others have demonstrated that the incumbents, who are focused on volume, can be disrupted by smaller producers and marketers. Eventually the bigger producers will lose their suppliers, or they will have to switch to higher quality inputs.

We all know that a fancy packet, such as those used by Silver Fern Farms, does not change the quality of the contents.

At the back of the report is a hit-list of 200 companies. Private equity and other offshore money has made a few plays, but there are a substantial number of high quality companies that are tightly held.

Some of my favourites, such as Balle Brothers, and Dairy Goat Farm, will never sell, but there are plenty of opportunities for those with very large check books. SSadly those investors are mainly from offshore, and New Zeaand has very little capital at work to support high growth businesses of any type. But that’s another issue.

Yes we can

It might take time, but the report does show that the farmers and growers will respond to market demand. The challenge is whether we can, as a society, help our food business ecosystem accelerate the change to owning the global high margin premium food position.

(Click to zoom)

RAW DATA: Coriolis' The Investors' Guide to the New Zealand Food and Beverage Industry (PDF here)

Lance Wiggs is the founder of Punakaiki Fund, which invests in high growth NZ based companies. He is a member of two Return on Science investment committees, and has helped more than 40 companies as an independent practioner through NZTE’s Better by Capital program. He writes at Lancewiggs.com

Sign up to get the latest stories and insights delivered to your inbox – free, every day.

Sign up to get the latest stories and insights delivered to your inbox – free, every day.