LVR impact is significant and growing

The Reserve Bank has released actual data on the extent to which banks are lending at 'Loan to Value' levels of 80% and above - the threshold imposed by the Bank Governor in October last year.

At the time the Governor stated that "From 1 October 2013, banks will be required to restrict new residential mortgage lending at LVRs of over 80 percent (deposit of less than 20 percent) to no more than 10 percent of the dollar value of their new residential mortgage lending".

Well the fact is that based on the months of December and January retail banks are not only keeping such lending below the threshold of 10% - they are actually barely touching 5% of the loans (by value).

In January just $147m of lending was made above the 80% LVR threshold representing just 4.8% of the total value of lending in the month. Accepting that January is a quieter month this amount represents a fall of almost almost 90% as compared to August last year.

What is interesting is the extent to which this significantly reduction of lending above the 80% threshold equates to in terms of the number of first time buyers in the market. For this analysis I have made some assumptions as full details are not available.

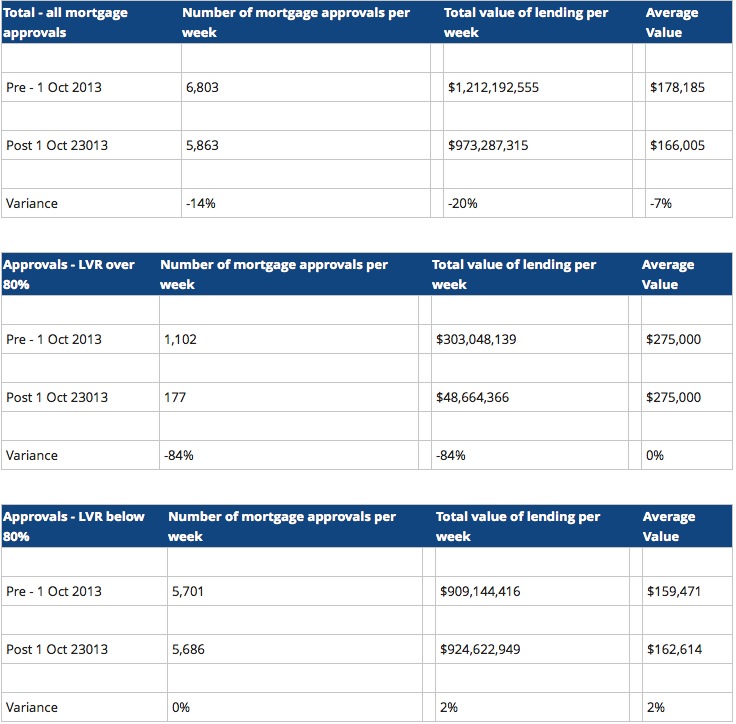

The data of weekly mortgage approvals published by The Reserve Bank shows the number and the total value and thereby the imputed average value. I have made the assumption that rather than thinking high LVR loans will be at a lower than average value, they are in fact more likely to be well above the average. The logic is that within this data set from the Reserve Bank of mortgage approvals is not just new loans but also refinancing of loans many of which may be older loans and thereby at a lower average value, whereas first home buyers representing a higher proportion of high LVR are likely to see loan values closer to say 80% of the median house price, thereby a loan of $330,000. For this reason I have assumed that high LVR loans have an average value of $275,00 whereas the average for all loans is closer to $175,000.

This table below sets out the overall data of the average of mortgage approvals for the 22 weeks pre 1st October and the 22 weeks since 1st October.

Based on the data and the assumption of high LVR loans, the data would seem to show that the massive reduction (close to 90%) in lending at high LVR represents a fall from around 1,100 such loans a week before the intervention of the Reserve Bank to an average of just 177 per week since the 1st October. Admittedly the last 2 months prior to implementation did likely see a degree of a 'lolly scramble" ahead of the changes.

The impact of this tightening of lending controls in the housing market has consequentially lead to the overall lending market being down 14% in the number of mortgage advances and 20% down in value, with the traditional lower LVR loans hardly changing in volume or average value across this period.

Clearly we only have 4 months data and the next few months will be most interesting to observe as to the trend, but at this point in time the data would seem to point to the view that the retail banks are being tighter in their implementation of the Reserve Bank's policy restriction than required - significantly impacting the property market.

Former Realestate.co.nz CEO Alistair Helm is founder of Properazzi.

Sign up to get the latest stories and insights delivered to your inbox – free, every day.

Sign up to get the latest stories and insights delivered to your inbox – free, every day.