Chorus has left the building

UPDATED with PHOTOS.

UPDATED with PHOTOS.

ABOVE: Telecom staff begin to gather for a separation ceremony at the company's recently Victoria St West, Auckland HQ. (Click to enlarge.)

ABOVE: Telecom gave Chorus managers pounamu as a parting gift. The "new" Telecom exec team were given high-viz vests by the ever-practical, cost-conscious Chorus. (Click to enlarge.)

Chorus chief executive Mark Ratcliffe address the crowd (click to enlarge).

Chorus staff leave the building - a largely symbolic move; most of the new company's employees never moved into the Victoria St campus, instead taking a new building in the nearby suburb of Newton.

ABOVE: Photos from Telecom's de-merger ceremony yesterday evening.

A TALE OF MARKET CAPS

Telecom pre-demerger: $4.9 billion

"New" Telecom market close yesterday: $3.8 billion

Chorus market close yesterday: $1.27 billion

Telecom 1990 privatisation value: $4.25 billion (inflation-adjusted: $7.02 billion

Source: Capital IQ

Telecom ceases to be

NOV 30: Today is Telecom and Chorus' offical separation date, following earlier approval for the network and wholesale division's spin-off by investors and the High Court.

Analysts have debated whether two companies will be worth more, or less, than one.

So far it's Even Stevens. Combined market cap has nudged up a little, tracking a little ahead of a broader market rise since November 23, when Chorus began trading.

On the eve of demerger, Telecom had a market cap of just over $4.9 billion.

At market close yesterday, Capital IQ gave Chorus a market cap of $1.274 billion, and Telecom $3.83 billion or $5.03 billion.

The main surprise has come from the allocation of value between the two companies, and the unexpected tilt in favout of "new" Telecom.

Pre-demerger, Forsyth Barr's Guy Hallwright saw Telecom (ex Chorus) worth around $3.17 billion and Chorus around $1.9 billion (with the proviso that pre-merger accounts, which did not detail all internal transactions, made it difficult to access the post-merger blance). Chorus listing price ($1.94) was also at the lower end of the range anticipated by the Grant Samuel valuation quoted in Telecom's demerger Scheme Booklet ($2.92 to $4.61).

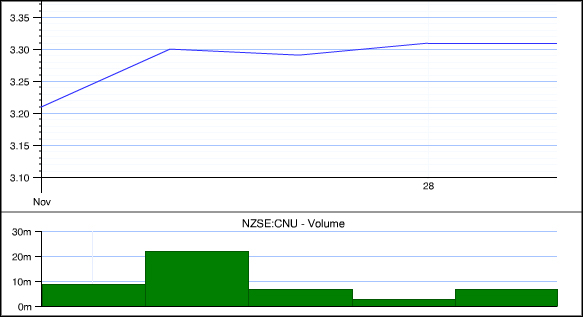

Chart courtesy Capital IQ. Click to zoom.

Chorus [NZX:CNU] debuted on the NZX on November 23 at $2.94. It shares closed yesterday at $3.30. Investors received one Chorus share for every five Telecom shares they owned. The spun-off company is expecting to pay an annual dividend of 25 cents per share for 2012 (which should work out to 15 cents, given demerger has taken place part way through the financial year). No dividend guidance has been given beyond 2012.

Telecom (ex-Chorus) shares [NZX:TEL] were adjusted to $1.94 on Novmeber 23. The closed yesterday at $1.99. The company has said it will continue its pre-demerger dividend policy of paying 90% of its net adjusted earnings for 2012. No dividend guidance has been given beyond 2012.

Telecom was hewn from NZ Post as a stanadlone state-owned enterprise in 1987, valued at $3.2 billion.

It's first true market valuation came in 1990, when it was privatised via its sale to US telcos Bell Atlantic (now part of AT&T) and Ameritech (today known as Verizon) for $4.25 billion (or $7.02 billion in today's dollars, according to the Reserve Bank's inflation calculator; increased competition has weighed heavily).

Telecom's share price soared over $9 in the late 1990s before crashing to earth with the end of the tech boom, and regulation that undermined its monopoly. Earlier this year, it hit all-time low of $1.96 before recovering to as high as $2.76 following what was seen as favourable Crown fibre outcome.

Shape of the new Telecom, Chorus

The wholesale-focussed Chorus is seen as a stable, regulated monopoly, reliably returning dividends.

However, Deutche Bank's Geoff Zame earlier noted to NBR that the company's outlook is complicated by interlocking variable costs such as the unknown speed with which people will take to fibre, which will in turn feed into the network build cost, cloud.

And while Chorus will have a lock on much of the nation's landline business (at least at the wholesale level) Rosalie Nelson, a market analyst with IDC, told NBR that faster wireless and cellular technologies, such as 4G/LTE, will increasingly emerge as fast broadband alternatives (although Sydney-based analyst Paul Budde told NBR there were, and would always be, practical limits to wireless).

Revenue, earnings

Telecom earlier divvied up its 2011 result between what will become two separate companies.

The company said that, on a pro forma basis, Chorus (including most of the division currently known as Telecom Wholesale) generated:

On a pro forma basis, "new" Telecom generated:

Debt allocation

New Chorus will take on approximately $1.7 billion of net interest-bearing debt (inclusive of associated derivatives) and New Telecom approximately $750 million to $950 million of net interest bearing debt (inclusive of associated derivatives), the company said in an earlier statement.

The upside for New Chorus is that its cap-ex will be eased by $929 million in taxpayer funds earmarked for the company under the government's $1.35 billion ultrafast broadband (UFB) project - 50% of which will be in non-voting shares (which will ultimately be repurchased by New Chorus), and 50% in interest-free debt. Assuming Chorus hits its deployment targets, the first repayments are not due until 2025.

Shape of New Chorus

The spun-off Chorus has its own CEO, Mark Ratcliffe, and its own board, as well as a separate listing.

The network and wholesale division is being "demerged" from Telecom as a condition of participation in the UFB.

Chorus won 74% of the UFB roll-out by premise.

Additionally, Christchurch winner Enable has a clause in its UFB contract allowing for a 50:50 joint venture with Chorus. On Friday, Enable chief executive Steve Fuller declined to comment on the possible joint venture.

Sign up to get the latest stories and insights delivered to your inbox – free, every day.