Just to demonstrate just how this change will impact insurance and homeowners' appreciation of the value of their home, let me take you through an example of a property which I visited at an open home recently.

The home In the highly popular suburb of Grey Lynn has a Capital Value of $870,000 which is made up of a land value of $590,000 and improvements of $280,000. These improvements are defined as the building and all that exists on the bare land.

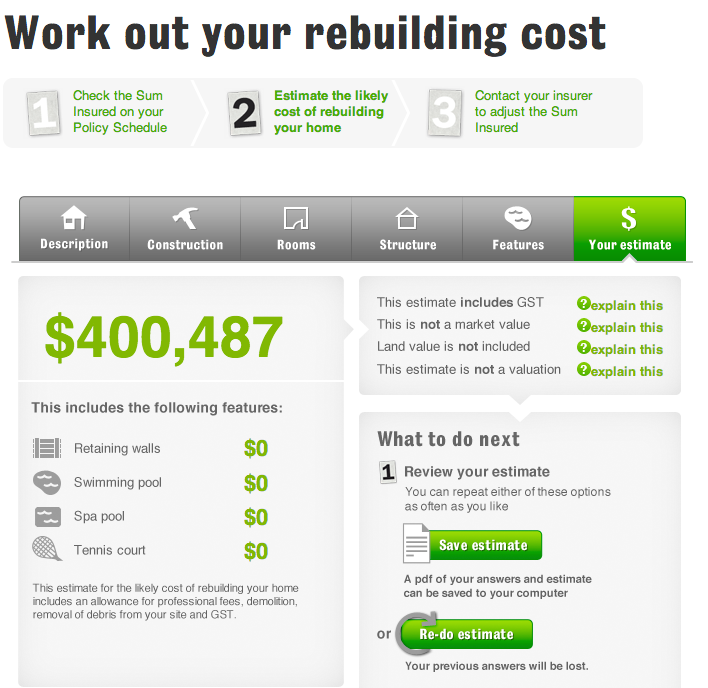

I went through the Home Rebuilding Cost Calculator to estimate the total cost of replacing this property. A highly detailed and lengthy exercise which does require a fair degree of appreciation of the details of your home’s construction.

The calculator came back with an estimate of $400,487 which includes GST and also an allowance for professional fees, demolition and removal of debris from the site.

Interesting that the CV for this property assessed the land at a value of $590,000 and the building at $280,000 yet the replacement cost of the building is estimated at $400,487. If the value of the land is appropriate (which is more likely to be the case) at $590,000 then the total 'value' of the land and building is very close to $1 million.

You are I am sure, interested to know the market value of the property today based on that well established notion of a "willing buyer and a willing seller". Well the property was sold recently for $1,395,000. This would therefore tells us that the value of land in this area is actually appreciated by 68% since the last assessment was undertaken in 2010/2011 – Auckland, or at least this area of Auckland is experiencing unprecedented demand.

Former Realestate.co.nz CEO Alistair Helm is founder of Properazzi.co.nz.

Postscript

I was prompted to write this article by the comment sent to me by a retired Quantity Surveyor who had read my article on why we should get rid of CV’s, he rightly asked the question as to whether people had considered what the long term effect will be on property / sales valuations once the insurance industry changes over to declared values for house insurance policies.

He stated that as he had his own construction business engaging in construction of architecturally designed houses & spec housing. Many of the houses that he built had construction costs of more than double what the current CV values were & he rightly wondered once owners start realising that replacement costs far exceed the CVs for their property, that they will start to try & negotiate selling prices based on replacement costs.

He reflected that this might well apply more to expensive architecturally designed properties, but in his experience all building costs usually exceeds CV values due too as most property valuations are based on historical values & consequently out of date.