While science received a modest top-up in the Budget this year, with a net increase of $50 million allocated to science and innovation initiatives, an intriguing tax provision aimed at helping start-ups engaged in R&D is potentially significant.

The scheme would allow small companies engaged in research and development to claim tax losses on that activity. Presumably it means that, for instance, software companies spending the first years of their existence as loss-making entities while they develop their products, could claim tax back against the amount of spending they do on researching and developing their software products.

You might be thinking that loss-making New Zealand companies don't pay any tax anyway - and you'd be right. As IRD explains:

"If a company's total expenses exceed its total income, it will generally have a loss for tax purposes. Companies in a loss position do not have to pay income tax."

So how will the tax break work - tax losses brought forward or converted to cash payments? No detail has been released about the scheme. But key questions will include:

- How is research and development defined?

- Will there be a limit on the amount that can be claimed in any one year or over successive years?

- Will IRD basically write a cheque to the start-up annually based on the taxed amount of the R&D it has done?

The UK's tax relief scheme for R&D allows small and medium sized companies engaged in R&D to claim tax relief on revenue expenditure:

"Generally, this means costs incurred in the day-to-day running of the business - not capital expenditure on assets."

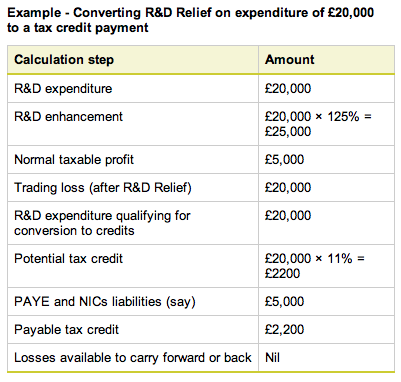

In the UK, R&D-related tax expenses, under certain circumstances, could be carried forward as tax loses or converted to tax credits as the below scenario illustrates:

Other costs eligible for tax relief in the UK scheme include employee salaries, contractor fees, materials, software and even fees paid to participants in clinical trials.

Revenue Minister Peter Dunne said in a statement that the scheme would encourage early-stage companies to spend more on R&D.

"That expenditure can be crippling for small ventures, given their capital constraints. With this proposal, we are effectively recognising that and looking to make sure these small companies are not disadvantaged".

Details of the proposed scheme will be released next month with a period of public consultation to follow. The SMC was unable to obtain further detail on the tax provision from Peter Dunne's office by press time.

Peter Griffin manages the Royal Society's Science Media Centre. He posts at SciBlogs.

Peter Griffin

Sat, 18 May 2013

Sat, 18 May 2013

© All content copyright NBR. Do not reproduce in any form without permission, even if you have a paid subscription.

BUDGET 2013: Detail slight on R&D tax deductions

29498