Infratil will stump up just over $A730 million for as much as 60% of Aussie radiology chain Qscan.

The Wellington-based investment company’s share price has walked back today’s NZ9c progress to trade at $5.60 since unveiling more details of its much-speculated first foray into healthcare.

Managed by Morrison & Co, Infratil confirmed on Friday it was part of a consortium in talks with private equity firm Quadrant to acquire its network of diagnostic imaging clinics.

The deal was “strategically and financially compelling” for shareholders, it has said.

A conditional offer worth $A735m was put on the table on Saturday by Infratil and Morrison’s Growth Infrastructure Fund.

The dual-listed company – which counts telco Vodafone New Zealand, cloud hoster Canberra Data Centres, and trans-Tasman renewables developer Tilt Renewables among its stable – will pay up to $A330m for a 60% stake.

Morrison’s infrastructure fund will take 15%, with the pair paying maximum equity of $A550m, according to an investor presentation. Debt facilities will fund the balance.

Infratil had total available liquidity of $609m at September 30 – mostly made up of $593m of undrawn debt. Gearing will rise to 30.1% following the transaction, from 25.5%.

“Qscan provides a high-quality entry point into a sector with structural long-term growth and potential to scale into a leading healthcare infrastructure platform,” Infratil chief executive Marko Bogoievski said.

“The Diagnostic Imaging sector benefits from long-term demographic tailwinds and technological advances that will allow it to play a growing role in the early detection of diseases such as cancer. Ultimately, increased investment in Diagnostic Imaging will reduce overall healthcare system costs while improving patient outcomes.”

Different avenue

Fat Prophets head of research Greg Smith said the acquisition was a change of tack.

“The company’s got a bit of a war chest from a few months ago, so, I don’t think they’re paying up or anything like that. The private equity sellers will probably be happy enough with their exit.”

The healthcare sector has been on a tear lately, Smith said, citing Fisher & Paykel Healthcare’s bullish run throughout the Covid-19 pandemic. Demand for radiology services and diagnostic imaging would only increase, given people’s rising health awareness.

“In terms of a defensive business, you’d probably say it’s right up there,” he said. “The price being paid, all said and done, doesn’t look too expensive. There’s quite a bit of room for growth still in Australia, with 70-odd clinics.”

Infrail could gain ground if it got more of a flavour for the sector but the price of any future deal had to be right, the analyst said.

“Investors are sometimes wary of rollups that are sold out of private equity and there’s been plenty of hiccups there in the past but with this one it does seem to be, on the surface, a fairly good-quality business and it doesn’t look like [Infratil is] overpaying so that should help ease any concerns.”

Strong record

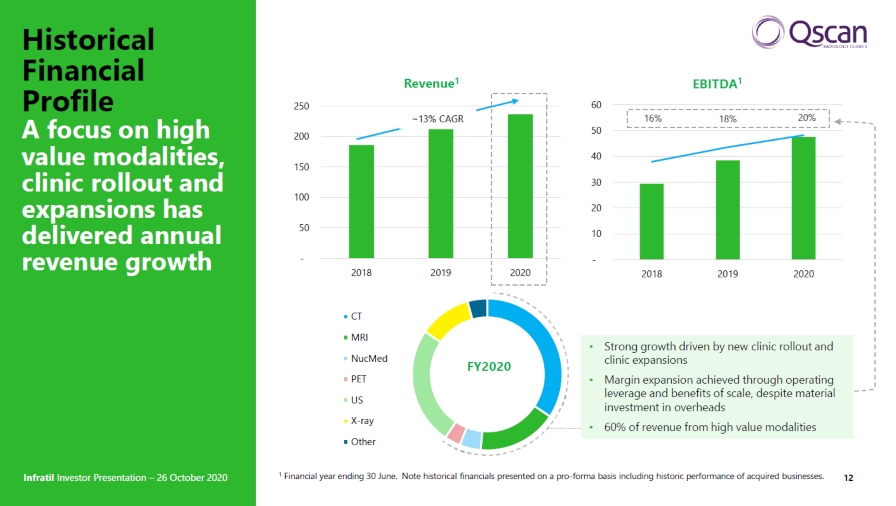

The price paid represents more than 12-times Qscan’s forecast earnings of $A52m to $A58m for the year to June 30, 2021.

Qscan’s current doctor and management shareholders must choose to retain the remaining quarter of shares for the deal to go ahead.

Should they have chosen otherwise by November 10, the transaction would fall away and the bidders could recover their costs.

However, Infratil expected doctors and management would sign up, with approval from Australia’s Foreign Investment Review Board the only other outstanding condition to satisfy by December 31.

Morrison’s head of Australia and New Zealand, Paul Newfield, said the market-leading Qscan was sitting in an industry primed to grow.

The business “has a secure revenue base backed by strong referral networks and a track record of strong, profitable growth, with significant further growth potential. Qscan is also known for the quality of its doctors and the strength of their sub-speciality expertise,” Newfield said.

Quadrant

First established in 2006, Quadrant’s business has transformed from a single clinic and hospital contract to a group operating some 70+ clinics across Australia, largely located in New South Wales and Queensland.

Within the network are 10 clinics offering positron emission tomography (PET) scanning, a technique commonly used in oncology and, together with MRIs and CTs, can show a more detailed picture of a body’s functioning, especially at a cellular level.

Qscan’s current business model sees it provide a complete infrastructure and services platform for radiologists, sonographers and support staff, who can concentrate on patient care.

The company owns all equipment, systems, contracts and licences while doctors are independent medical practitioners, and it collects bills and keeps a service fee before sending clinicians an agreed revenue share.

Quadrant has been asked for comment.