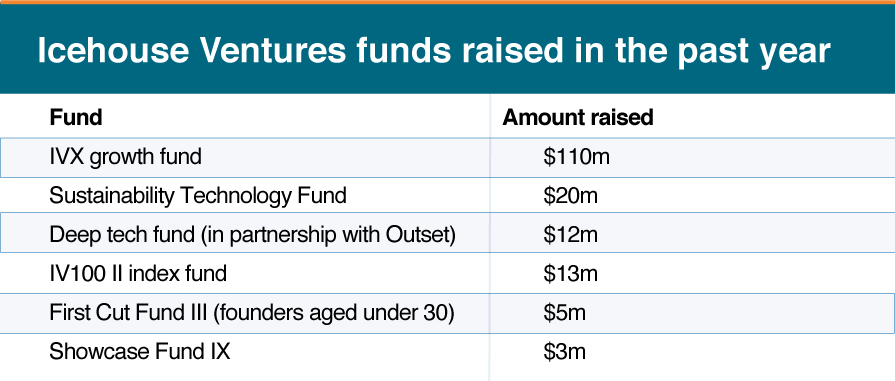

Auckland venture capital firm Icehouse Ventures has raised $110 million for its first growth fund, IVX, which closed on Friday.

The fund minimum had been set at $50m and Icehouse Ventures chief executive Robbie Paul said they had expected to raise around the $75m mark.

KiwiSaver scheme Simplicity, which is an investor in Icehouse Ventures, committed $20m as anchor investor to the fund, while other large backers included Warren Couillault’s Hobson Wealth Partners and Harbour Asset Management.

Paul said the fund also attracted a number of cashed-up Kiwi founders who had recently exited their companies and expatriates keen to support local companies.

While it was never easy raising money, Paul said he was happy with where the growth fund got to.

“There are just more examples of great Kiwi companies emerging and more evidence that great Kiwi companies can generate high-value returns for investors,” he said. “I also think IVX is among a number of funds that are giving investors more options to participate in that space that they didn’t previously have and that’s part of the growth.”

The switch

Icehouse Ventures has had a plethora of seed-stage funds (it has been culling the names of some, including Tuhua under the Icehouse brand, with a third seed fund due to be raised next year).

It has invested a total of $210m into 265 companies since its existence, including its angel groups. Icehouse Ventures started out in 2003 when Ice Angels set up as the country’s first angel group and the first Icehouse fund emerged in 2013. In 2019, the company attracted investment from Simplicity, Jarden, and Sir Stephen Tindall’s venture investment arm, K1W1.

Paul said it had $205m in managed funds from 1200 investors, of which $90m is still to be invested while it was on track to invest $70m this year, double its record $35m last year, across 90 companies.

It was among the first investors in startups – including Mint Innovation, Crimson Education, Ask Nicely and First AML – which allowed it to invest further in each of their growth rounds but it has typically stuck to investing at the seed stage in Kiwi startups.

“We will continue to do that at scale. What this [IVX]fund does is pick up where our early-stage funds leave off and continue to invest in the small number of companies that emerge as growth-stage companies and have generated revenue, have built teams, and are scaling offshore,” Paul said.

The fund is aiming at companies that have successfully raised Series A rounds of more than $5m.

While it is not limited to companies the venture capital firm has already backed, only three of the fund’s 16 investments didn’t fall into that camp. Four more investments are due to close this month.

IVX investments include Dawn Aerospace, Crimson, Joyous, Halter, Tradify, Shuttlerock, Spalk, The Insides Company, and Mentemia.

IVX aims to invest in about 30 companies within three years and provide follow-on investment to the portfolio until the startup founders hit exit. The 10-year fund will pay out investors an aggregate return as each company exits.

Co-opetition, not competition

In the past few years, there has been a rise in the number of venture capital companies active in New Zealand, including several from overseas, and government-backed NZ Growth Capital Partners also doing direct investments as well as backing other funds.

Paul said there were many investors keen to invest in this space but, typically, they and his funds don’t go it alone.

“We’ve co-invested with every named and brand venture fund in this country as well as many of the offshore funds who have an interest in New Zealand,” he said. “There is a lot of collaboration in this space so I would phrase it co-opetition rather than competition as more often than not, people see value in collaborating and sharing the load around and bringing collective experience and networks to the table to help these companies.”

Icehouse Ventures didn’t apply for funding from NZGCP’s $300m Elevate Fund as Paul said it had sufficient private sector backing that allowed it to run its own investment strategy. Elevate has invested $157m so far into six venture funds.

Increased capital

The increased amount of capital around has meant Icehouse Ventures is sometimes not the lead investor in these growth companies, something Paul said it wasn’t concerned about unless leading the investment gave it terms or allocations it wouldn’t have otherwise achieved.

Another reason to lead the investment round or seek a board seat would be if there was evidence it would “disproportionately benefit” the companies that it was backing, he said.

“Part of the IVX thesis, and we do lead and we’ve led about half of the companies so far, is that actually once a company is five years old, has 50 employees, and is still demonstrating that they have more growth ahead of them than behind them, they can pick and choose the investors they want from around the world.

“And so, often that means they’re able to find lead investors who have more relevant stage, geographic, or industry experience than we could bring. So long as we’re co-investing on the same terms, and we have, and we’re aligned to the same outcomes, we are happy to co-invest and have others lead.”

One recent example was LawVu, a Tauranga-based tech startup that makes cloud-based software for in-house legal teams. It raised $17m in a Series A funding round in August led by New York-based high-growth venture capital firm Insight Partners along with Australian venture capital firm AirTree Ventures.

“We were happy to be along the journey alongside them in this most recent round,” Paul said, with the money raised supporting LawVu’s ongoing growth plans in the US.

The risk element

With more competition and co-opetition, valuations for startups have been on the rise, with founders able to force better terms.

Paul said valuations had gone up from pre-seed to Series D across the board and were not recognisable to what they were five or 10 years ago.

“They are still a fraction of what other markets are showing. So I’ve never subscribed to the idea that New Zealand is a bargain. But, on paper, you could suggest that it is still by comparison to other markets.”

He thinks the venture market is still “less inflated” than the rest of the investment asset classes out there.

While higher valuations put more risk on investors getting the returns they’re seeking, Paul said he wanted to correct the narrative that investing in risky startups means investors will lose their money.

While riskier than a term deposit, venture capital investing shouldn’t be framed in the same way as an individual making an angel investment for the first time, he said.

“The only reason I think that narrative needs to be debated is because too often it’s projected by a single individual who invested in his or her nephew’s company, gave the company too much money on the wrong terms, then gave more money in a subsequent round without asking questions and then lost their money.

“Yes, these type of bloodbath stories happen and they will continue to happen all the time. But there’s a big difference between investing once in an asset class or in a company that you don’t understand and investing in a portfolio of 30 to 48 companies that have essentially distanced themselves from a pack of more than 250 companies that we’ve backed.”